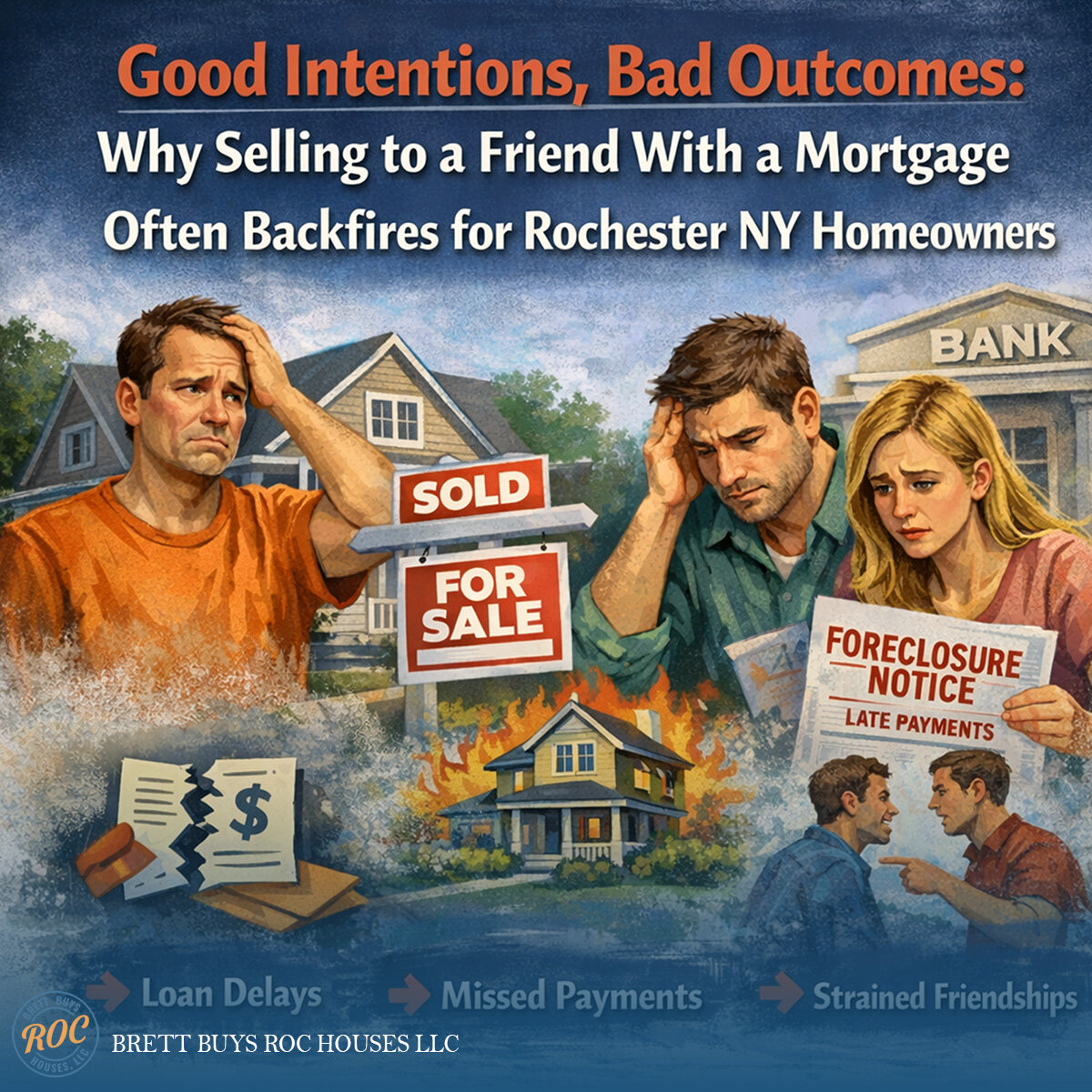

Some of the most stressful home sales I’ve seen in Rochester, NY didn’t involve strangers.

They involved friends, neighbors, or family members.

When someone you trust says, “I want to buy your house,” it feels safe. Familiar. Easy. But once a mortgage is involved, good intentions stop protecting the seller.

Banks don’t care about relationships—and they don’t rush because of them.

Why Emotional Deals Are the Hardest to Fix

When a loan-based deal involves a personal relationship:

- Sellers hesitate to push deadlines

- Buyers avoid uncomfortable conversations

- Problems get ignored instead of addressed

- Time quietly slips away

By the time reality sets in, the seller has already lost leverage.

When “We’re Just Waiting on the Bank” Becomes Dangerous

This is the most common phrase we hear from sellers who call us too late.

Behind the scenes, that usually means:

- The appraisal is delayed or low

- Underwriting is stuck

- Additional documentation is being requested

- The buyer’s financial profile has changed

None of these are in your control as the seller.

Relationship Strain Is an Unspoken Cost

When delays happen:

- Sellers feel stuck

- Buyers feel pressured

- Resentment builds

- Communication breaks down

What started as a friendly arrangement can end in frustration, damaged relationships, or legal tension.

New York Adds Another Layer of Risk

In NY, once contracts are signed:

- Attorneys control the pace

- Missed deadlines can create legal exposure

- Extensions are not guaranteed

Mixing legal obligations with personal relationships is risky—especially when money and time are tight.

Real Example: A Friendly Deal That Nearly Cost a Home

A Rochester homeowner accepted a friend’s loan-based offer and waited over 80 days. During that time:

- A foreclosure timeline continued

- Backup buyers moved on

- The loan was ultimately denied

By the time the seller reached out to us, options were limited and more expensive.

Why Professional Cash Buyers Reduce Emotional Risk

A professional buyer:

- Sets expectations clearly

- Makes decisions upfront

- Removes banks from the equation

- Keeps relationships out of legal risk

This isn’t about pressure—it’s about protection.

FAQs – Selling to Friends & Mortgage Risk

Is it risky to sell to a friend using a loan?

Yes. The risk isn’t the person—it’s the financing.

Can personal relationships speed up loan approvals?

No. Banks follow process, not personal timelines.

What happens if the loan fails late in the process?

You lose time, leverage, and often other buyers.

Can I keep things friendly while protecting myself?

Only by setting strict timelines and backup plans from day one.

Is it awkward to ask for proof of financing from a friend?

It may feel awkward, but it’s necessary. Wanting to buy is not the same as being able to buy.

Why do sellers wait too long before pivoting?

Because emotional comfort often overrides financial reality—until it’s too late.

If you’re balancing relationships, timelines, and financial pressure—clarity matters.

Visit brettbuysrochouses.com

We’ll help you evaluate certainty versus risk, without pressure or judgment.