One of the most common questions homeowners ask is: can I sell my house while in forbearance?

The short answer is yes.

Forbearance pauses or reduces your mortgage payments temporarily. It does not prevent you from selling the property. However, before listing or accepting an offer, it’s important to understand how repayment works and what options are available once the forbearance period ends.

Selling may be one solution — but it is not the only one.

What Forbearance Actually Means

Forbearance is an agreement with your lender that allows you to temporarily stop or reduce payments due to hardship.

It does not:

- Forgive the missed payments

- Eliminate accrued interest

- Cancel your mortgage

Instead, the paused payments must eventually be addressed through repayment, modification, deferral, or payoff.

That’s why many homeowners begin asking, can I sell my house while in forbearance, as their reinstatement period approaches.

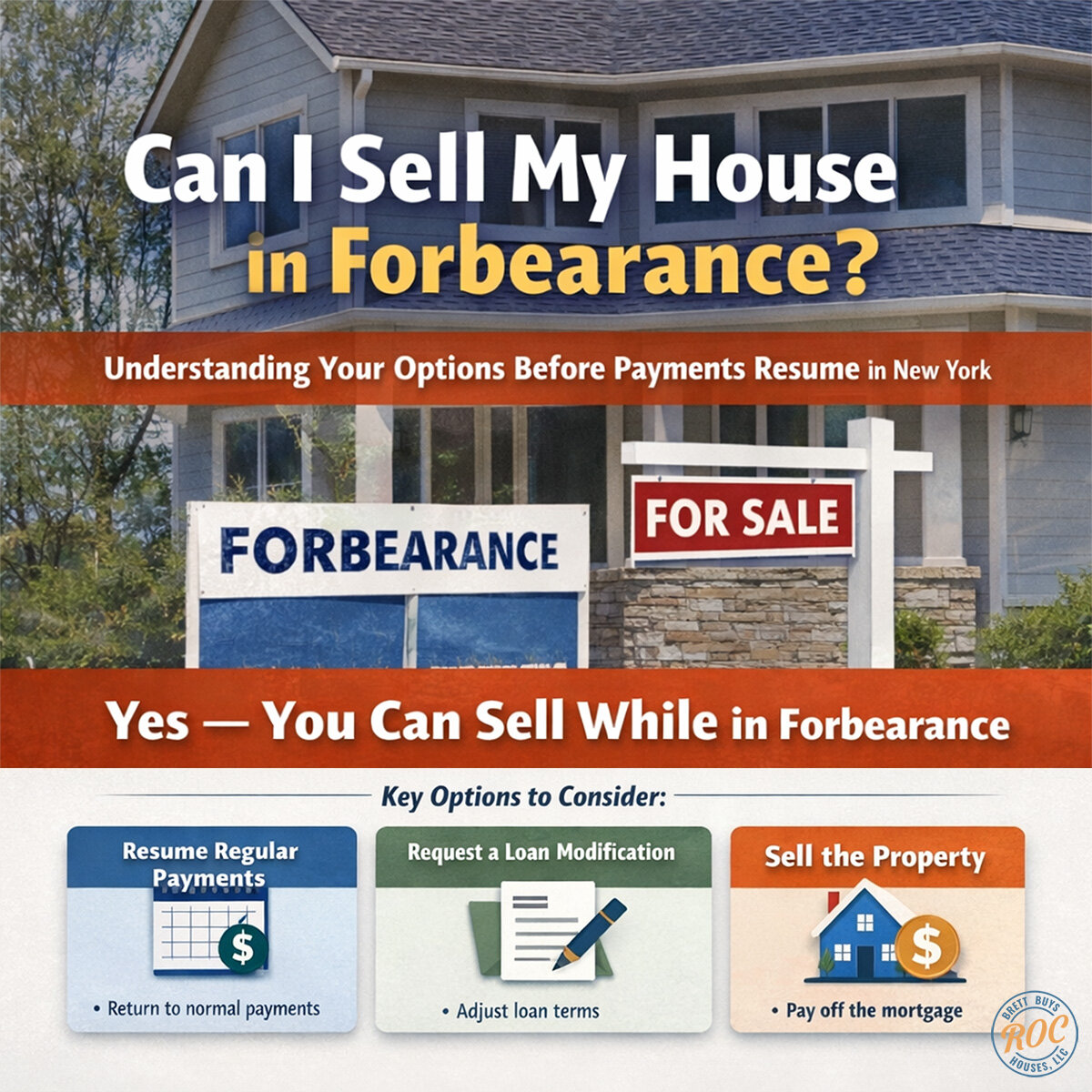

Option 1: Resume Regular Payments

In some cases, homeowners are able to resume standard monthly payments once the hardship ends.

Depending on your lender, missed payments may be:

- Added to the end of the loan

- Structured into a repayment plan

- Included in a loan modification

If your income has stabilized and equity remains strong, keeping the property may be a viable path.

Option 2: Request a Loan Modification

If resuming full payments immediately feels difficult, a loan modification may reduce your monthly obligation or restructure the loan balance.

This process requires:

- Income documentation

- Financial review

- Lender approval

Modifications can take time and are not automatically approved. It is important to evaluate whether long-term affordability improves under modified terms.

Option 3: Sell the Property

For many homeowners, selling becomes the cleanest exit strategy.

When you sell:

- The mortgage balance is paid off at closing

- Deferred payments are included in the payoff

- Accrued interest is satisfied

- The lien is released

If the property has sufficient equity, selling can eliminate the debt entirely and provide remaining proceeds.

That is why homeowners frequently asked because selling may allow them to reset financially without entering default.

What If Equity Is Limited?

If home values have increased since your purchase, you may have enough equity to sell and cover the full payoff.

If equity is limited, the situation becomes more complex. In those cases, options may include:

- Negotiating with the lender

- Exploring short sale discussions

- Reviewing hardship alternatives

Before making a decision, requesting a current payoff statement from your lender is critical. That number includes:

- Principal balance

- Deferred payments

- Accrued interest

- Any applicable fees

Clarity on your true payoff amount determines your next step.

Timing Matters Before Payments Resume

Forbearance periods eventually end. When they do, lenders expect a structured plan.

Selling before default begins provides more control. Waiting until payments lapse or foreclosure proceedings start reduces flexibility. If you are asking “can I sell my house while in forbearance”, the better question may be: “What does my timeline look like before repayment begins?”

Proactive action preserves options.

Frequently Asked Questions

Will selling hurt my credit if I’m in forbearance?

Selling and paying off the mortgage typically does not harm credit, especially if the loan has not entered default.

Do I need lender approval to sell?

No special permission is required to sell, but your lender must provide a payoff statement for closing.

Can I sell to a cash buyer while in forbearance?

Yes. The payoff process is the same — the loan balance must be satisfied at closing.

What happens if I do nothing?

Once forbearance ends, missed payments must be addressed. Ignoring the situation can lead to delinquency and eventual foreclosure.

Final Thoughts

If you’re wondering “can I sell my house while in forbearance”, the answer is yes — but the right decision depends on your equity, income stability, and long-term goals.

Selling is one option. Modification is another. Resuming payments may also be viable. The key is understanding your numbers and timeline before pressure increases.

Need Help Reviewing Your Options?

At Brett Buys Roc Houses LLC, we work with Rochester homeowners navigating forbearance situations and help them understand all available paths.

If you’re evaluating whether selling makes sense, we can review your property, discuss your equity position, and outline realistic options.

Visit brettbuysrochouses.com or Call (585) 585-299-9709